CHICAGO – In times of crisis, repayment prioritization of credit products often provides a clearer view of how consumers are meeting the financial burdens they face. A new TransUnion (NYSE: TRU) Global Payment Hierarchy study found that the COVID-19 pandemic had a pronounced effect – in a short period of time – on how people paid their debts, particularly when faced with financial stress. In the United States, the changes were prominent across multiple credit products, with consumers clearly prioritizing their mortgage loan payments over auto loans and credit cards.

This study is unique in that it highlights how and why payment dynamics changed in different countries as a result of the COVID-19 pandemic – a global crisis that has impacted consumers worldwide.

“TransUnion has tracked payment hierarchy dynamics for more than a decade, including how these patterns changed in the U.S. following the Great Recession and in many other countries when they have encountered localized financial challenges,” said Charlie Wise, head of global research and consulting at TransUnion. “This study is unique in that it highlights how and why payment dynamics changed in different countries as a result of the COVID-19 pandemic – a global crisis that has impacted consumers worldwide. These insights will better equip both financial institutions and consumers, fostering more trustworthy interactions between them as the world begins to normalize and recover from the pandemic.”

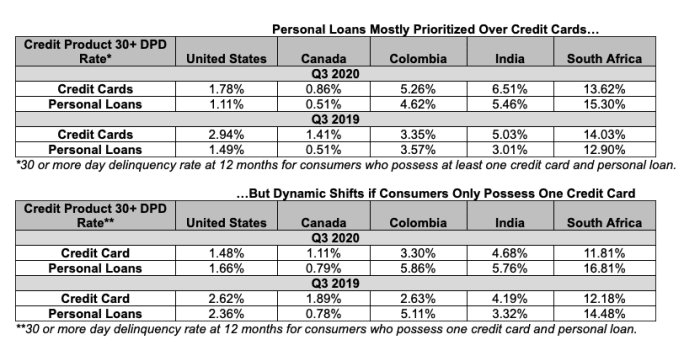

Credit Cards v. Personal Loans – What is the World Prioritizing?

TransUnion analyzed and compared trends for wallet profiles that are popular across the countries studied, including the United States, Canada, Colombia, India and South Africa. The study observed within each country those consumers with one or more credit cards and at least one personal loan, to identify if any changes took place in the payment hierarchy. To determine which credit product was prioritized over the other, TransUnion observed payment performance of the credit products over a 12-month time period, including whether or not one of the credit cards or personal loans went at least 30 days delinquent.

In the U.S., the study observed that personal loans were prioritized when consumers possessed multiple credit cards, though the gap between delinquency rates—indicating the degree of preference—narrowed during the pandemic. Similar trends were seen in Canada and India, which suggests that credit cards took on increased importance during the pandemic and that consumers were more focused on keeping their cards in good standing by making timely payments.

A flip in the payment hierarchy happened during the pandemic in South Africa as credit cards were prioritized over personal loans, reversing the pre-pandemic hierarchy in favor of personal loans. Colombian credit usage showed no clear prioritization of either product until March 2020, when more value was placed on personal loans.

An interesting dynamic occurred in the U.S. and other countries wherein the payment hierarchy flipped for those consumers possessing only one credit card and at least one personal loan. In those cases, credit cards were prioritized during the pandemic, in contrast to the pre-pandemic preference for personal loans. In the U.S., this particular group comprised approximately 20% of the overall study population. This shift further demonstrates the increased importance of credit cards for consumers during the pandemic and the need to maintain access to this valuable source of credit. For those consumers with at least one credit card and at least one personal loan, on average, U.S. consumers possess three credit cards and one personal loan.

“Cash was clearly not king during the early parts of the pandemic. Millions of people opted to use their credit cards to make digital transactions from the safety of their home for groceries, clothes or other everyday items,” said Matt Komos, TransUnion’s head of research and consulting in the U.S. “If you only have one credit card and you were worried about visiting stores at the height of the pandemic, there’s a strong likelihood you will preserve that card to continue spending and making digital transactions. If you possess three cards, though, it’s far more likely that you will go delinquent on one of them before you do so with a personal loan if you are facing financial hardship, as many consumers can continue to get by as long as they have access to at least one card.”

These findings were corroborated by a global survey of 2,667 consumers who possessed credit products in Brazil, Canada, Colombia, Hong Kong, India, South Africa, the United Kingdom and the United States. Consumers across the globe recognized that there will be consequences if they miss at least one payment of any of their credit products. For instance, more than half (53%) of global respondents with a credit card said they expected to receive a call from their lender if they missed one payment.

The negative implication of a missed payment to a credit score was understood most by credit card and personal loan holders. Approximately 68% of credit card holders and 65% of consumers with personal loans said a consequence of a missed payment would result in a lower credit score. Comparatively, consumers with auto loans (55%) and mortgages (57%) were not as aware of this consequence.

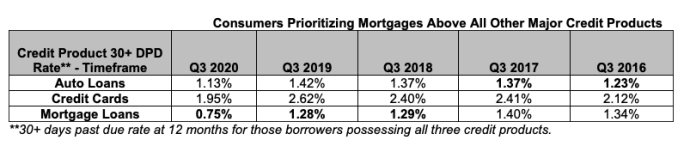

Deeper Dive Into U.S. Payment Hierarchy Dynamics Shows Mortgage is Priority #1

In the U.S., TransUnion also conducted a payment hierarchy study focusing on the three most popular credit products in the country – auto loans, credit cards and mortgages. Approximately 27.8 million consumers held all three loans as of Q3 2020, and mortgages were clearly prioritized over the other credit products. This dynamic has held true since Q4 2017.

The pandemic, though, has caused even greater prioritization of mortgages over the other credit products. For those consumers possessing auto loans, credit cards, and mortgages, the 30+ days past due delinquency rate at 12 months following observation was lowest for mortgages, at 0.75%, as of Q3 2020. Auto loans had the second lowest delinquency rate at 1.13%, followed by credit cards at 1.95%. This is very likely connected to the growth in home prices over the last several years as housing markets across the country have remained strong, and consumers’ desire to protect the equity in their homes. As well, as lockdowns and the shift to work/school from home permeated during the pandemic, keeping current on home loan payments took on increased importance in 2020.

“Mortgage is once again the clear priority for U.S. borrowers,” said Komos. “The mantra, ‘you can’t drive your home to work’ doesn’t have the same effect when millions of Americans are waking up, showering, eating breakfast and taking only a few steps to their home office.”

In addition to more people working from home and rising home values, mortgage loan performance is likely benefitting from thousands of mortgage borrowers entering accommodation programs soon after the onset of the pandemic. The study points to both subprime and near prime credit risk mortgage borrowers benefitting the most from these programs as they were able to delay payments and maintain their accounts.

Similar to the global study comparing credit card and personal loan performance, prioritization of payments shifted if a consumer possessed only one card. Of the 27.8 million U.S. consumers in the study possessing an auto loan, credit card and mortgage, only 5.3 million people had one credit card in their wallet. For this subset of the population, mortgage remains the clear priority, but consumers with only one credit card valued it more than their auto loan beginning in Q2 2020. This shift suggests the heightened importance of maintaining access to at least one credit card as online commerce and digital transactions have become a daily necessity for many U.S. households.

Survey data highlight that U.S. consumers valued their mortgages over other loans because the credit product has the highest perceived value of all expenses. Furthermore, six in 10 U.S. consumers expected to receive a call from their lender if they missed one mortgage payment and more than half (52%) said their missed payment would have a negative impact to their credit score. Nearly one in five consumers (17%) said they would experience foreclosure or their home would be repossessed if they miss a mortgage payment.

“The pandemic has changed so much in the world, but understanding why consumers are making important credit decisions only serves to better help the lending ecosystem in the future,” concluded Komos.

To learn more about consumer payment prioritization shifts during the pandemic, register for TransUnion’s April 22 webinar here. For more information about TransUnion’s Global Payment Hierarchy Report, please click here.